Many of us have filed our 2016 taxes already, but there are some looking to wait a little longer. Does it seem that doing your taxes raises more questions than answers. Did you do the right things last year to maximize your return? What can you do this year to make the 2017 return the best yet.

And what if you've taken the plunge and said "I Do" and now there's two of you? Margie Archer, CRPS®ADPA®, First Vice President – Investment Officer, Portfolio Manager from Wells Fargo helps us answer some of the "What do I do with my taxes now that I'm a married gay man" questions.

Federal Taxes and Same-Sex Marriage: How should you file?

Marriage equality is the law of the land in all 50 states. In a historic decision on June 26, 2015, the U.S. Supreme Court struck down state bans on same-sex marriage, resolving a civil rights debate that has raged for more than four decades. The decision grants LGBT couples the same rights as other couples with regard to health insurance, child custody, medical decision-making authority, and more. It also levels the tax-filing scenario for same-sex couples who choose to marry.

The New Choices

In the past, same-sex married couples living in states that didn’t recognize their marriage had extra requirements when filing income tax returns. Typically, that meant filing federal tax returns as a married couple and state tax returns as single/unmarried individuals. That increased the time, effort, and expense of filing.

Now, those same couples can simply file as married, either jointly or separately, at both the federal and state level. But does simply checking a different box on your tax forms guarantee a better outcome? Not necessarily.

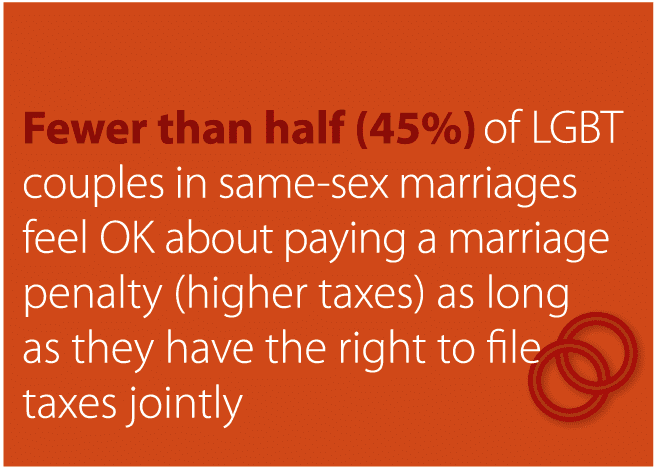

If you and your partner earn roughly the same amount of money, filing jointly could bump you into a higher tax bracket – a circumstance known as the marriage penalty. On the contrary, if one spouse earns little or no income, and the other is the primary wage earner, filing jointly may result in a marriage bonus. In other words, by tying the knot, you may wind up owing Uncle Sam less than if you remained single. *

Domestic Partnerships and Civil Unions

It’s important to keep in mind the Supreme Court’s recent ruling applies only to same-sex married couples, not to registered domestic partnerships or civil unions. Although a handful of states recognize domestic partnerships and civil unions, the IRS does not. So, while these designations may offer some of the same rights and responsibilities available to married couples, it’s only at a state level and on a state-by-state basis.

Tax Benefits That Apply to All

What’s become clear since the Supreme Court’s decision is same-sex married couples grappling with how to file their tax returns can’t count on a one-size-fits-all solution. However, here’s what you can count on:*

- The ability to transfer an unlimited amount of assets to your spouse, free from federal gift or estate taxes, either during life or at death.

- The right to leave your spouse property upon your death that doesn’t come with a heavy estate tax bill due to the unlimited marital deduction.

- More tax-planning options upon inheriting your spouse’s retirement account.

- The right to open an Individual Retirement Account on your spouse’s earnings record, if you are unemployed.

Indeed, the tax benefits afforded to same-sex spouses are finally on par with those of heterosexual spouses. If you’re already married or thinking of getting married, do take the time to talk with your tax advisor to see how your marital status might impact your income tax and your financial future as a married couple.

Timing Your Marriage to Minimize Taxes

Choosing a wedding date that accommodates family, friends, and employers — not to mention the church and reception hall — is a wedding planner’s greatest challenge. So should you also consider Uncle Sam when selecting a date?

Your tax filing status is determined on December 31 of each year. For tax purposes, that means even if you wait until the last day of the year to walk down the aisle, the IRS will consider you married for that entire year. If there is a notable disparity between your and your partner’s income, then getting married by December 31 could benefit your tax situation. However, if your combined income pushes you into a higher tax bracket, you may want to marry January 1 of the following year to avoid a negative impact on your current-year tax bill.*

Income isn’t the only factor that influences whether marriage will result in a tax penalty or bonus. Answering questions such as who incurs deductible expenses, who can claim children as dependents, and what tax preferences you might qualify for can also help you gauge the potential effects of marriage on your tax situation—and enable you and your partner to determine the best time to exchange vows.

* Our firm does not provide legal or tax advice.

Thanks Margie Archer for the great tips. Take it as you like, but as always, seek out counsel of someone you trust.

Does Margie's advice match what you have heard before?

What other advice have you received about filing after your nuptials?

We did, indeed, file as a

We did, indeed, file as a same-sex legally married couple on our Federal income tax return, the first year it was available (we do not have state tax in Texas). We did incur higher taxes because of our combined income, and I can tell you, we were more than happy to pay our fair share of taxes for the right to be recognized the same as opposite sex married couples always have been!